Bank Reconciliation Statement: Examples and Formula

Sometime such checks are not honored because the person issuing the check does not have sufficient funds in his account. In such situation, bank reverses the entry and reduces the balance of depositor’s account to previous amount. All transactions between depositor and bank are entered by both the parties in their records. These records may disagree due to various reasons and show different balances.

Step 2: Review the deposits and withdrawals

After adjusting the balances as per the bank and as per the books, the adjusted amounts should be the same. If they are still not equal, you will have to repeat the process of reconciliation. When David writes out a check, he makes an entry on the credit side of his cash book (being a reduction in asset, cash at bank). When an account holder issues a cheque, which the bank pays, the bank debits the account holder’s personal account.

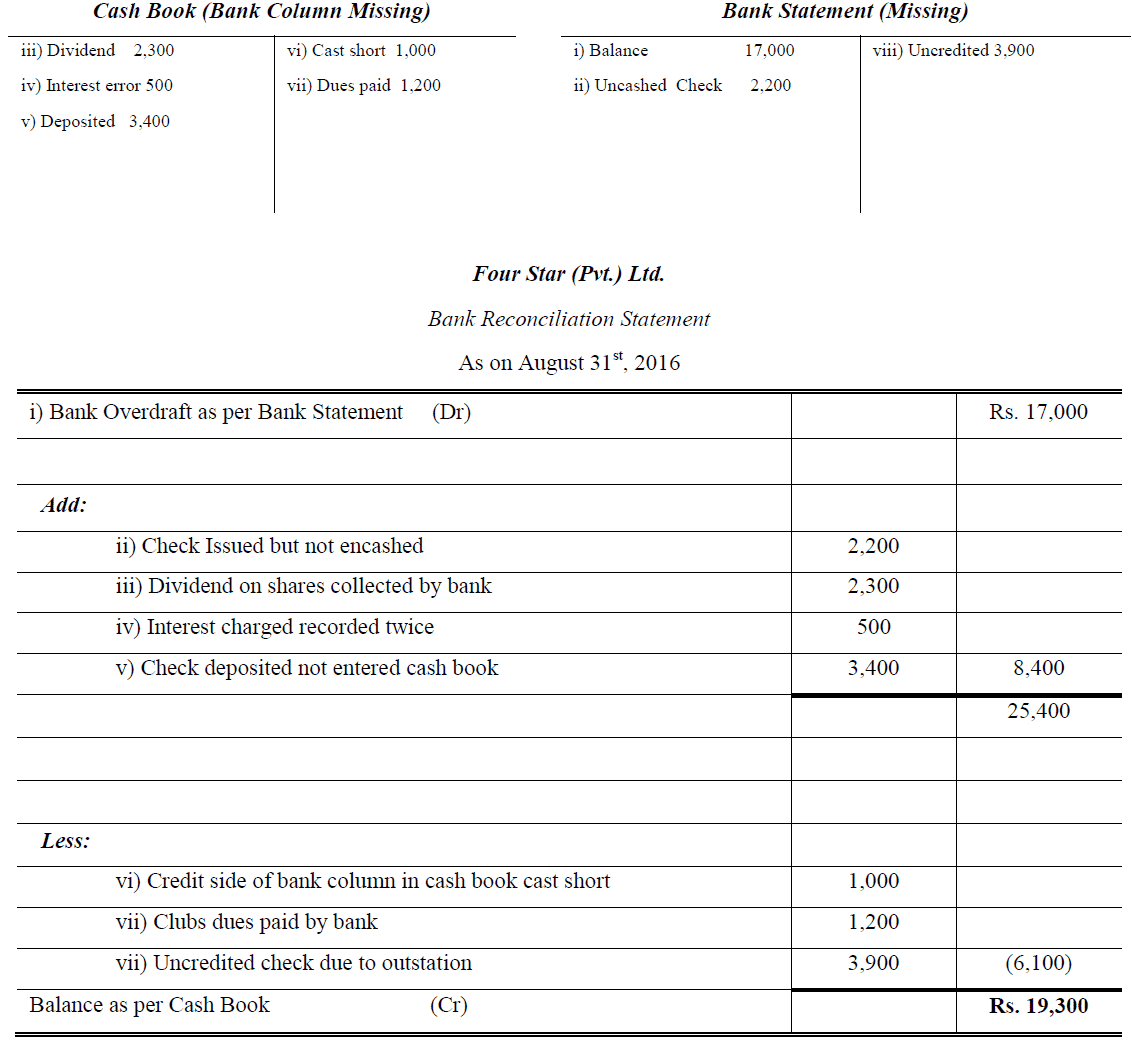

Example #2 of Bank Reconciliation Statement Template

FreshBooks accounting software helps you track income and expenses and generate reports and financial statements. Try FreshBooks for free to streamline your tax preparation and bank reconciliations today. One of the most common causes of discrepancies in bank reconciliations is delays in deposit and transaction processing. Checks sent or received at the end of the day, or toward the end of the quickbooks undeposited funds account explained month, may be subject to delay which will prevent them from being included on the bank statement. Accounting for these delays is key to reconciling the total amounts on the company’s financial statement and the bank statement. The cash account balance in an entity’s financial records may also require adjusting in some specific circumstances, if you find discrepancies with the bank statement.

To Ensure One Vote Per Person, Please Include the Following Info

They can also be helpful when reconciling accounts for pulling reports.Another example would be where you deposit cash, but the teller doesn’t post it correctly. You have to go back and compare your records with the bank’s to try and figure out what went wrong so you can correct your records to match the banks. The bank will debit your business account only when they’ve paid these issued checks, meaning there is a time delay between the issuing of checks and their presentation to the bank. These time delays are responsible for the differences that arise in your cash book balance and your passbook balance.

Step 3: Adjust the bank statements

- In such situation, bank reverses the entry and reduces the balance of depositor’s account to previous amount.

- A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

- A bank reconciliation statement is only a statement prepared to stay abreast with the bank statement; it is not in itself an accounting record, nor is it part of the double entry system.

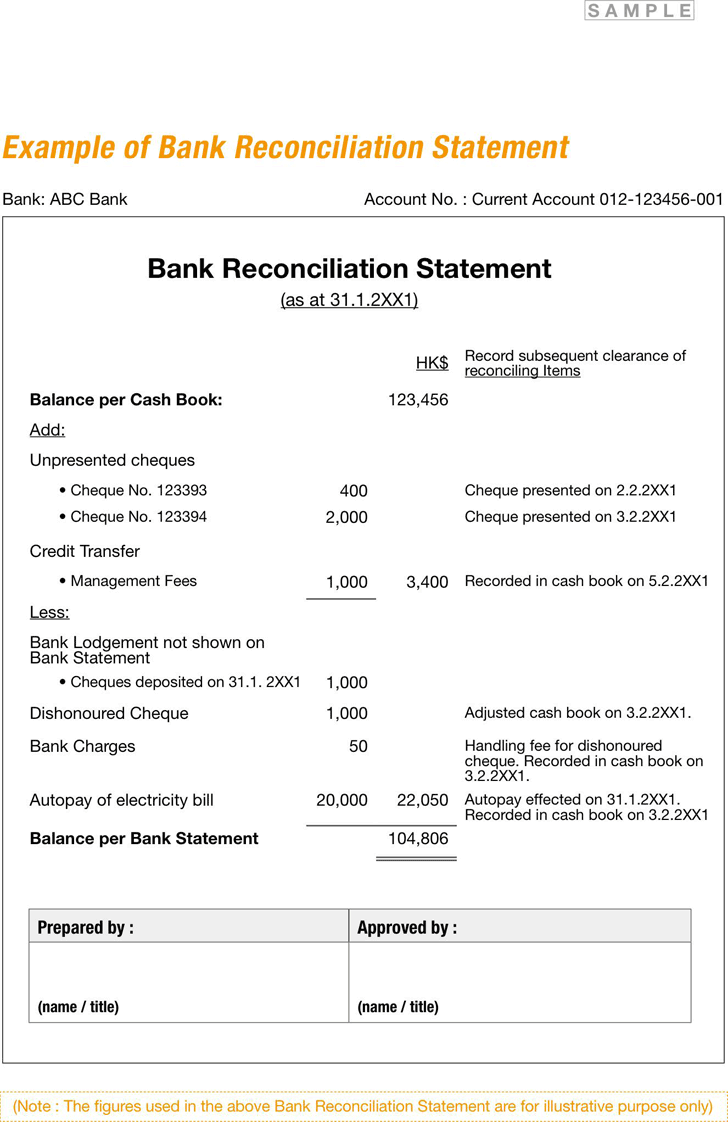

- Additionally, the bank records all deposits received from David in the credit column of his statement of account.

Deposits in transit, or outstanding deposits, are not showcased in the bank statement on the reconciliation date. This is due to the time delay that occurs between the depositing of cash or a check and the crediting of it into your account. In cases where you discover discrepancies that cannot be explained by your financial statements, it’s best to contact your bank. It’s possible that a banking error has occurred or that you have been charged for something you were unaware of. If the charges are not from your bank, the bank can also help you identify the source so that you can prevent any fraud or theft risk. Performing immediate bank reconciliations for large cash amounts or suspicious transactions further increases your ability to catch fraud and error.

While reconciling your books of accounts with the bank statements at the end of the accounting period, you might observe certain differences between bank statements and ledger accounts. If this occurs, you simply need to make a note indicating the reasons for the discrepancy between your bank statement and cash book. Typically, the difference between the cash book and passbook balance arises due to the items that appear only in the passbook. So it makes sense to record these items in the cash book first in order to determine the adjusted balance of the cash book. Once the adjusted balance of the cash book is worked out, then the bank reconciliation statement can be prepared.

As a result, the balance shown in the bank passbook would be more than the balance shown in your company’s cash book. When your business receives checks from its customers, these amounts are recorded immediately on the debit side of the cash book so the balance as per the cash book increases. However, there may be a situation where the bank credits your business account only when the checks are actually realised.

Nowadays, all deposits and withdrawals undertaken by a customer are recorded by both the bank and the customer. The bank records all transactions in a bank statement, also known as passbook, while the customer records all their bank transactions in a cash book. Conducting regular bank reconciliation helps you catch any fraud risks or financial errors before they become a larger problem.

A bank statement shows you those transactions and enables you to capture them in your records to reflect all the transactions affecting your business. The main reason a business should reconcile its bank statements is because you need to ensure your cash balance on the balance sheet is accurate. Regular bank reconciliations also help prevent fraudulent or unauthorized transactions from going unnoticed. A company’s cash balance at bank and its cash balance according to its accounting records usually do not match. This is due to the fact that, at any particular date, checks may be outstanding, deposits may be in transit to the bank, errors may have occurred etc. Bank reconciliation is the process of comparing accounting records to a bank statement to identify differences and make adjustments or corrections.

The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site.

In order to prepare a bank reconciliation statement, you’ll need to obtain both the current and the previous month’s bank statements as well as the cash book. When David deposits money with the bank, he makes an entry on the debit side of his cash book. Additionally, the bank records all deposits received from David in the credit column of his statement of account.